Manufactured homes – or mobile homes, as they were designated up until 1976 – come in a variety of designs. What they have in common across locations is often scorn for their existence. Whether it is disdain from the media, negative judgments about the residents, or outright prohibition by zoning and legislative measures,1 there are a shortage of communities that welcome a mobile home park within their boundaries.

Manufactured home communities, part of nearly every municipality in the United States, are left out of the housing crisis conversation despite their affordability. Given the recent news about the Tar Heel Mobile Home Park, it is poignant to discuss the state of manufactured housing communities in our country. In order to learn more, I sat down with Michael Stegman, Senior Fellow in the Housing Finance Program at the Center for Financial Markets at the Milken Institute, who founded the Center for Community Capital in 1997 while chair of UNC’s Department of Public Policy.

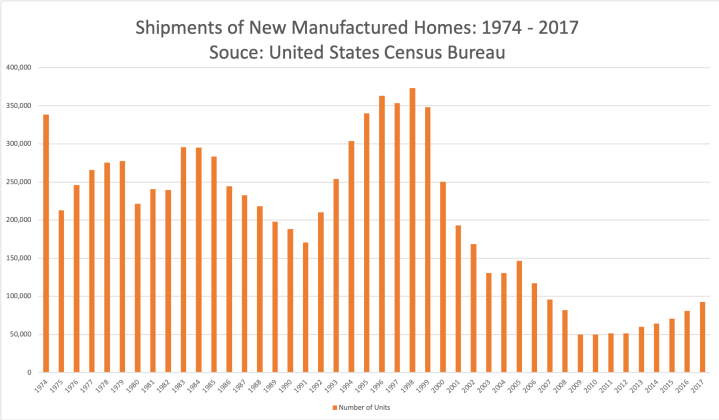

The history of manufactured homes traces back to World War II when it was used as an efficient and cost-effective housing solution for both war-related workers and returning veterans.2 Before the 1940s, mobile homes had offered an affordable option for families during the Great Depression.3 By the 1950s, the houses had become less mobile, larger in size, or more frequently attached to the land.4 Dr. Stegman explained that in the 1970s, the manufactured housing industry was shipping over 300,000 units a year nationally.5 This declined by the early 2000s, when the number of manufactured housing units shipped dropped to half that number, reaching a record low in 2009.

According to the U.S. Census Bureau, 19% of the manufactured housing market was shipped to Texas in 2017. Alabama is second, with 7% of manufactured homes located within the state. In most states, those who purchase manufactured housing have the opportunity to title it as real property (similar to a mortgage on a single-family site-built home) or personal property (also called a chattel loan, which is closer to a loan used to purchase a vehicle).

Manufactured housing has remained an affordable alternative, a salient note given the affordability crises across the country. National nonprofits have endorsed manufactured housing as a viable solution, among them the Corporation for Enterprise Development (CFED), the National Consumer Law Center (NCLC), the Housing Assistance Council (HAC), and NeighborWorks America.6 In 2016, the average price per square foot for a new single-family site-build home was $107, compared to $43 for a single-wide manufactured home and $51 for a multi-section.7 Dr. Stegman offered background on why this housing option, though more affordable, is not the easy solution one might hope.

“There really is no national manufactured housing policy,” Michael Stegman elaborated. “In a broader context, we don’t have a national affordable housing policy that focuses on the supply. Increasingly, we are experiencing supply constraints and shortages, particularly at the starter home and lower priced tiers.”

Manufactured housing represents one of the few affordable housing production options in our country. Dr. Stegman qualified this by noting that our national housing policy has shifted to primarily focus on rental assistance and housing vouchers for low-income families for existing housing units, rather than affordable housing production programs. “The low income housing tax credit is the largest subsidized production program providing equity to for-profit and non-profit developers,” he explained, although this is a smaller impact in comparison to the housing voucher program that helps families afford rent.

“There are two real constraints to manufactured housing,” Dr. Stegman explained. “First is the placement of units. Zoning and land use controls make it uneconomical to place a home on urban land or difficult to change the zoning.” Regulations on minimum lot size might also mean that the resident might not be able to afford to land required for the home. “About a third of manufactured homes in the country are in land-lease communities,” Dr. Stegman elucidated. In this instance, the resident owns the manufactured home but rents the land. The manufactured home is set up on a concrete pad on the land, and is often incredibly difficult and expensive to move, rendering more contemporary homes less mobile. These residents in land-lease communities are at a high risk of displacement; a mobile home landlord can receive more cost-effective offers to sell their land to developers, leaving the residents without a place to live.

The issue manufactured homes and land leasing is playing out here in the Town of Chapel Hill. “For historical reasons, all manufactured housing has been located on the fringe of the town’s urban development,” Dr. Stegman said. “However, the Town has since grown into and incorporated these areas, in the space between urban and commercial.”

Dr. Stegman pointed out that there are plenty of manufactured housing communities in the area that are not noticeable, such as a community on Weaver Dairy Road and Martin Luther King Blvd. “Altogether, they make up about 200 units and are mostly occupied by two-income, Latinx families with kids,” Dr. Stegman explained. “It represents the cheapest form of housing but they are threatened by development.” The 13.9-acre Tar Heel Mobile Home Park was sold to a private developer, the previous owner hoping to salvage as many mobile home plats as possible, accomplished through the community members petitioning the Town for help.8 The Town of Chapel Hill was featured on an international blog by ESRI for the use of “partnerships, engagement, and the ArcGIS mapping software to prioritize Town-owned land for new affordable housing development.”9

Despite their affordability, manufactured housing faces a crisis regarding preservation of their communities. This problem of preservation stems from the costliness of moving the homes in conjunction with the uneconomical solution of developing new manufactured housing parks, which is often not feasible without city participation or subsidy.

The second major constraint for manufactured homes after placement is financing. “The work that we are doing at the Center for Community Capital focuses on the financing constraints,” Dr. Stegman responded. In order to understand the true weight of the financing impact for the manufactured housing industry, you have to understand the role manufactured housing played in the affordable housing crisis. Professionals in housing cannot forget the 2007 sub-prime mortgage and foreclosure crisis; however, in the 1980s and 1990s, we experienced a similar crisis in the manufactured housing financing space. “Most manufactured housing loans are personal, or chattel loans,” Dr. Stegman explained. “These are loans the lender provides to the resident, and the home itself is the only property held as security. If you can’t pay the loan back, the bank can repossess the home.” In most states, in order to obtain a mortgage, the recipient must own the land; if the recipient defaults on the manufactured home loan, then they owe the lender the home and the land.

“For historical reasons, the manufactured housing sector financed the majority of its loans through personal loans,” Dr. Stegman continued. At the height of the manufactured housing industry after around 1991, “Fannie Mae and Freddie Mac were buying securities backed by bundled chattel loans as well as securities and mortgages.” At this time, there were very few lenders who bundled these loans, created securities, and sold those securities to investors, and Fannie Mae and Freddie Mac were among the biggest investors. They also had a higher interest rate than mortgages, which is still true to this day. The increase in demand for manufactured housing in the 1980s and 1990s prompted lenders to make loans to families who could not afford them. Dr. Stegman connected this trend to the sub-prime crisis of 2008, stating that “If you go back and study what happened in the manufactured home finance in the late 1980s and early 1990s, it looked a lot like 2008.” Fannie Mae was hit particularly hard financially went this bubble burst, and both Fannie Mae and Freddie Mac completely extricated themselves from this industry by the late 1990s.

“There is virtually no secondary market for manufactured housing loans in the present day,” Dr. Stegman concluded. “Anyone who buys those loans is in the primary lending market. What’s important about the secondary market is that the process frees up monday for the primary market to make more loans.” This means that the manufactured housing finance market does not benefit from the financial lending opportunities the same way that single-family site-built homes currently functions, limiting the ability for new units to be produced.

This second constraint, more so than the location of manufactured homes, is the true obstacle for manufactured homes becoming a true solution to the affordable housing crisis, according to Dr. Stegman. There is a serious disadvantage for potential homebuyers from a lower income bracket who cannot take advantage of the financial benefits or asset-building in the same way as a site-built home. “It’s harder to get a loan on a used manufactured home than a new one. It’s harder to refinance a manufactured chattel loan if interest rates go down,” Dr. Stegman elaborated. “In a normal mortgage market, you can refinance to save money,” he explained further, noting that the absence of an active secondary market is a detriment to this affordable housing solution.

Dr. Stegman explained that the Center for Community Capital is primarily exploring the finance side of manufacturing housing, learning from consumers who have recently bought manufactured homes to understand their financing decisions. There is a multitude of questions – whether they obtained a mortgage to buy the home, procured a chattel loan, purchased the land, or even had the choice between the types of loans. Fannie Mae and Freddie Mac have been out of the market for almost 25 years and will need to ascertain the market experiences of consumers to understand if it is worth resources to re-enter this market.

On the legislative side, HUD may be looking at modernizing regulations with the support of Clayton Homes, one of the largest manufacturers in this industry.10 Dr. Stegman had not heard of any progress to date but noted that an overhaul of this magnitude would be a “multi-year process” in order to “take a serious look at streamlining or modifying [regulations] that wouldn’t reduce safety but might make it more economical,” aligned with this administration’s interest in de-regulation.

For the sake of communities like Tar Heel Mobile Home Park, planners should hope that the private sector, financial institutions will see an interest in manufactured homes. If they do, then it is up to planners to solve the placement issue of the manufactured housing puzzle.

Featured Image: Modern Transportable House. Source: Wikidepia Commons.

Dr. Michael A. Stegman, now a Senior Fellow in the Housing Finance Program at the Center for Financial Markets at the Milken Institute, founded the center in 1997 while serving as chair of UNC’s Department of Public Policy and MacRae Professor of Public Policy and Business.

Dr. Stegman’s interest in asset-building strategies for low-income Americans and communities grew while serving in the Clinton Administration as assistant secretary for policy development and research at the U.S. Department of Housing and Urban Development. Since founding the Center, Dr. Stegman has served as a counselor for housing finance policy at the U.S. Department of the Treasury, as the director of policy and housing for the MacArthur Foundation, at the Bipartisan Policy Center in Washington D.C., and as a senior policy adviser for housing for the National Economic Council in the White House.

About the Author:Emily Gvino is a first-year master’s student seeking dual degrees from the Department of City and Regional Planning and the Gillings School of Global Public Health. Her research interests involve how the built environment can address social justice issues and the impact of climate change and the environment on health. Prior to UNC, Emily earned her bachelor’s degree in urban & environmental planning and Spanish at the University of Virginia.